Why Token Models Are the Key to Building Robust Digital Economies

Why Token Models Are the Key to Building Robust Digital Economies

Nearly every crypto project is priced based on its token, but not all of them are created equal.

by Adam Kreitzman, intern

Introduction

At the core of every crypto project, regardless of its application, is a token that in theory gains value with increased use of the platform. This token not only allows investors and early adopters to have a stake in the success of the project, but it's also the very lifeblood that keeps the project operating.

So what determines the value of these tokens? There are a lot of answers to this question, and models for token value accrual are constantly changing, even in established projects. While some projects have found success with a variety of methods for token utility, others have fallen by the wayside due to broken mechanisms that tied their tokens to the platform or rampant inflation caused by the minting of new tokens to create artificially high staking APRs.

In the DeFi space, there are some fairly complex models such as ve (Voting Escrow) tokens, as well as other methods of token locking that are designed to align incentives for a community. However, we will focus mainly on the tokenomics of layer 1 protocols, layer 2 protocols and some DeFi applications that have seen success with simplistic incentive alignment.

One thing is clear: there is no one-size fits all model for designing token models. Some may be versatile, but for the most part, Layer 1s, DeFi apps, GameFi apps, and other miscellaneous blockchain applications all have different ways of designing tokens to harmoniously sync with their ecosystem.

Brokenomics

Luna (Terra) and Ohm and its forks are two examples of tokens that grew massively but failed ultimately due to their tokenomics.

1. Terra

Terra was a popular alternative Layer 1 protocol that was built using the Cosmos SDK with a token called Luna. It gained massive traction in large part due to its native algorithmic stablecoin called UST (TerraUSD). UST and the Luna token were inextricably linked due to a mechanism which allowed 1 UST token to be burned for the equivalent of 1 dollars worth of the market price of Luna and vice versa. There was also a heavy incentive to deposit UST tokens on Luna-native Anchor protocol which allowed people to receive an average of 20% APY on their UST, facilitated by the minting of new tokens.

The major issue was that aside from this algorithmic swap mechanism that “pegged” UST to a dollar, the only thing that was backing it was a protocol-owned treasury consisting of several non-stable crypto assets such as Bitcoin.

The price of Luna surged in 2021 as people wanted the “stable” yield from UST that was comparatively high, reaching over a 40 billion dollar valuation at its peak. However, on May 5th, 2022, the price of UST depegged from a dollar, and the sell pressure on UST overwhelmed both the Luna redemption mechanism and the single-digit billions of buy pressure from the Luna treasury that attempted to stabilize the peg. Roughly 60 billion dollars of market capitalization between Luna and UST evaporated almost instantaneously, and the Terra project which at one point seemed to some to be the most promising layer 1 protocol outside of Ethereum (though, to others, a coin that was destined to fail from the outset), died overnight.

2. OHM

Another example was the Ohm token from OlympusDAO, which attempted to create a reserve currency backed by its own treasury that ensured at least a 1:1 redemption rate between an OHM token and Dai.

By design, the Ohm token would have a price floor of 1 USD but theoretically have much more upside. People were enticed to join by massive APRs that were generated through the minting of new tokens. This was partially by design, as the staking APR was meant to offset changes in price due to increased token supply, and while this worked for some time, the combination of speculative mania over receiving 4 to 5 digit staking APR (which was all inflation) as well as a whale selling off their tokens to create cascading liquidations caused a crashed in the token price. This example showed that using rampant inflation to attract liquidity can have disastrous consequences, particularly if those who are buying in are unaware of where the yield is actually coming from.

Because of its early success, many projects forked Ohm codebase and tried to adapt it to different use cases. Two examples of this were Wonderland (which was a version of OlympusDAO that was ported to Avalanche) and KlimaDAO which was an Ohm fork that wanted to create a reserve currency of carbon offsets. Both of these adaptations, along with many other forks that gained less notoriety, all met a similar fate.

Creating a proper token model is difficult, as it requires carefully considering the desires of all users of a platform and trying to engineer a system with parity that rewards all users for their contributions. On top of this, it requires a model that is sustainable over the long term, and there are minimal examples of token models that have proven successful over a long period of time. Poor implementations can lead to devastating outcomes down the line even if there is success in the short term, as we saw with the Terra Luna debacle.

Layer 1 token models

Layer 1s have several methods of driving value to its native token, but the one that is fairly standard is using the token as gas. Using the native token to pay for blockspace, with the cost going up in response to congestion, allows blockchains to burn tokens from its supply and counteract emissions to either validators or miners. Therefore, as usage of the blockchain increases, people are required to buy its native token in higher amounts to process transactions, naturally driving value to the token.

Not only are these tokens the gas that power the blockchain, but oftentimes they are used to price the value of the ecosystem itself because much of the liquidity for tokens is paired with the native blockchain token. This is why we oftentimes see TVL (Total Value Locked) as a metric for determining whether or not a blockchain’s token is over or under-valued. As projects on top of blockchains grow, token price will follow as there is more demand for paired liquidity between projects and the native blockchain token.

Additionally, with proof-of-stake blockchains, users typically have the option to stake their tokens in order to gain yield in return for validating the network. However, this would more accurately be considered a tax on those who do not validate the network since the yield is coming directly from protocol emissions.

Most of the prominent layer 1 blockchains follow this model, with their own twists to give their blockchain and native token unique value proposition.

1. Ethereum

Ethereum for instance, follows this methodology and is able to create a deflationary token by burning more tokens in fees than it emits in staking validator rewards. This is in large part because of Ethereum’s massive fee generation relative to other applications.

Ethereum’s steep transaction fees are what spurred the creation of alternative layer 1s, but an interesting paradox has arisen as a result, as revenue generation and sustainability have come into the limelight within crypto. New chains such as Avalanche, Solana and several others have created scalable networks that can process thousands of transactions per second (compared to Ethereum’s 14) with far cheaper gas fees. While these chains have seen immense user growth over the past couple of years, most are not generating nearly enough revenue to balance out validator rewards, and thus are quite inflationary as a result. This becomes a catch 22 as chains want to be cheap and scalable to attract new users, but if transactions are too scalable and cheap then they no longer manufacture significant revenue, which is why alternative L1s have begun taking other approaches to token value accrual.

2. Avalanche

One example of this is with Avalanche, whose team is attempting to build a horizontally-scaling infrastructure called subnets. Their SDKs allow for people to launch their own custom layer 1 blockchains that are then validated by a subset of mainnet validators. In order to launch a subnet, however, the subnet creator needs to be a mainnet validator themselves, which requires staking at least 2000 AVAX tokens. In theory, as demand for subnet infrastructure grows, there will be more demand for AVAX tokens which are subsequently removed from circulation. While Avalanche was among the blockchains that some referred to as “ETH-killers”, the team dubs the chain as “layer 0 infrastructure” instead, as it facilitates the creation of application-specific chains.

Download Free Vectors | Vector69")

3. Polkadot and Cosmos

Avalanche is not the only protocol that attempts this, either. Both Polkadot’s network of parachains and Cosmos’ Internet of blockchains are different adaptations of this framework, as both have a main chain with several interconnected sidechains, but the usefulness of the native tokens DOT and ATOM is not as well-defined outside of security and validation of the main blockchain. Cosmos’ native ATOM token is supposedly going to see upgrades to its value accrual with the launch of ATOM 2.0 in the future, as it has been criticized for the lack of token utility in the past. While having these systems to launch interoperable and scalable blockchains that are specific to a use case is beneficial for the growth of the blockchain ecosystem as a whole, it is not immediately clear that launching app-specific chains will drive value to the native token of the whole platform, especially if the new chains use their own tokens for gas costs. It is a balancing act for layer 0 infrastructure to draw in developers to expand their ecosystem whilst also driving value to their platform without making it too cost-prohibitive so that they look elsewhere. Lastly, there have been suggestions that new projects may consider airdropping tokens to those who stake the native-layer tokens in an effort to build community, but so far this is just a theory.

3. Solana

Solana, on the other hand, is a perfect example of the scalability conundrum. As of now, it is among the fastest blockchains with a max TPS (Transactions Per Second) north of 2000. However, Solana does not generate much in fees despite being the blockchain that processes the most transactions, averaging close to 45K in fees the last 7 days, compared to 6.8 million dollars in fees for Ethereum. While Solana’s speed and scalability is beneficial for its users, it also leads to an inflationary setup as burned transaction fees are easily outweighed by protocol emissions.

So while alternatives to Ethereum are seemingly low-revenue and inflationary, this is not necessarily a catastrophic situation for them. People tend to view each chain as its own digital economy with the native token acting as a base unit of money. So, increases in chain-usage, tradable pairs, and locked liquidity are all catalysts that can overcome inflationary pressures in the near term.

An interesting dynamic that has evolved is the competition between alternative layer 1s and layer 2 protocols to attract users and capital from those in search of cheaper transaction fees.

Layer 2 Tokenomics (or lack thereof)

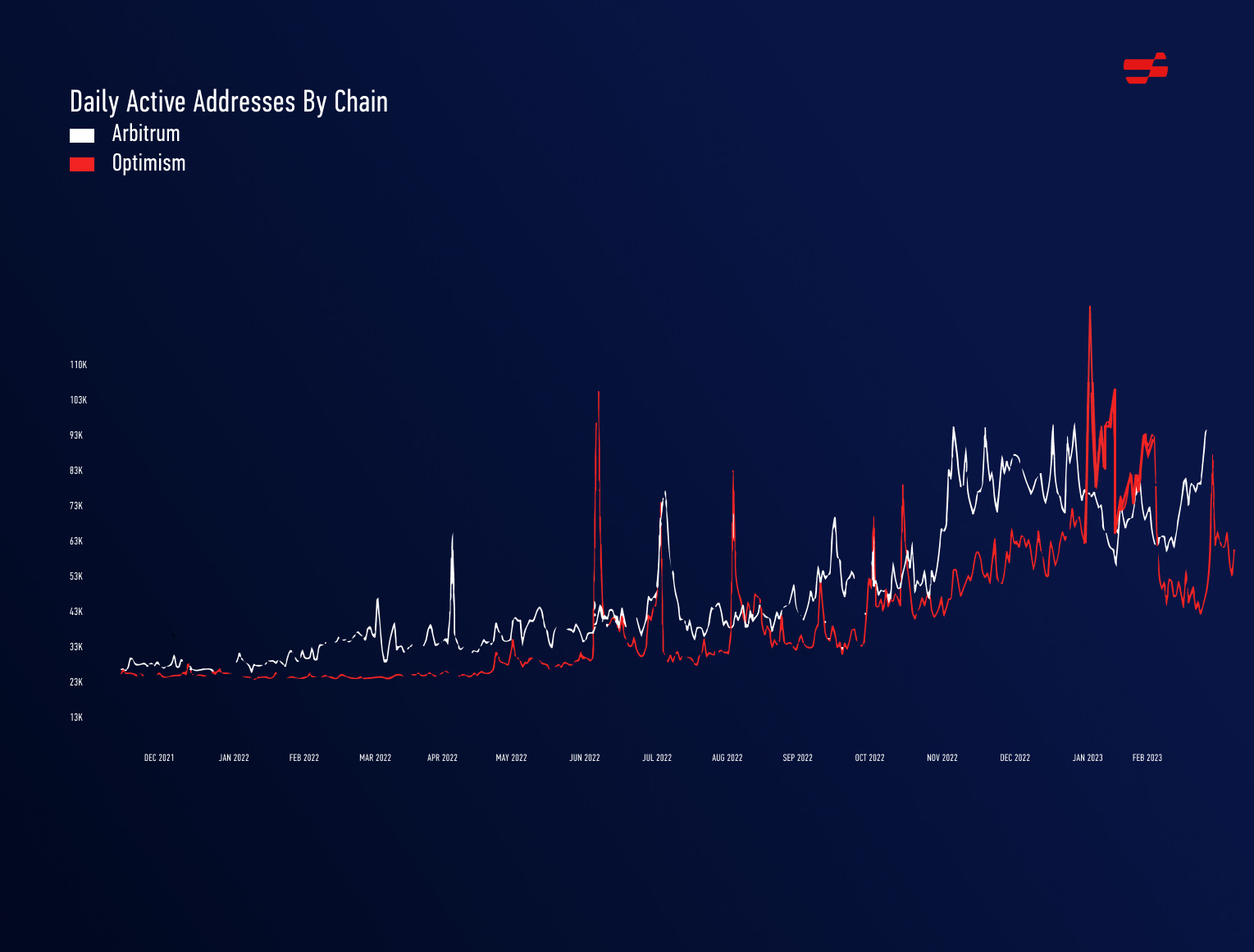

The top two layer 2 protocols by TVL are Arbitrum ($1.99B) and Optimism ($1.04B). Between these two, only Optimism has a token. Arbitrum has yet to launch a one, though it has been heavily rumored that they might in the future.

The layer 2 conundrum is a bit different in this case, as rather than worrying about scalability leading to lower fees, L2s have to decide between using their own token and ETH as gas. L2s may feel pressure to burn ETH as their stated goal is to scale Ethereum, but doing so is detrimental to the utility of their own token.

Arbitrum vs. Optimism

Nothing illuminates this more than the differing outcomes of Arbitrum and Optimism thus far. Arbitrum and Optimism are similar mechanically, as both are optimistic rollups that utilize ETH for gas, but Optimism decided to launch a token early on while Arbitrum did not.

Optimism’s usage surged after a community airdrop of its token, OP, coupled with quests that allowed people to earn OP through on-chain actions. While this attracted many users, it also attracted yield farmers and wash traders who were looking for arbitrage opportunities in the ecosystem. This inorganic growth did not stick, however, as there was a steep decline in active Optimism users directly after the end of Optimism quests.

On the other hand, without a token to incentivize activity, Arbitrum relied on dApps, UX and cheap fees to gain users. Arbitrum’s fees are currently cheaper than Optimism, and its growth in users and TVL has been a big byproduct of successful applications built on it, with GMX, a decentralized derivatives exchange, in particular accounting for more than 25% of the TVL on Arbitrum.

The following chart depicts the active users of each platform, with Optimism’s radical peaks being driven by yield-farming opportunities, compared to Arbitrum’s growth seeming to be more organic and sustainable. With that being said, Optimism has still maintained some traction, additionally having a native DEX called Velodrome (a fork of Solidly), which accounts for a major amount of TVL.

If Arbitrum has become the L2 with the highest TVL rather quickly with no token incentives while fostering several innovative DeFi applications, it raises the question of whether an L2 which uses ETH as gas actually needs a token at all. After all, the L2 with the most success to this point in attracting liquidity didn’t need one. But, proponents of an Arbitrum token believe a community airdrop will increase the liquidity available on the chain and draw even more interest from users, while also offering the additional upside of token incentives to attract even more builders and users to the platform. And perhaps the least sanctimonious reason to expect an Arbitrum token is that it was developed by a company called Offchain labs, which received heavy outside funding, and launching a token is one possible way for them to return value to their investors.

Examining all the non-Ethereum smart contract platforms tells a similar story, regardless of whether it is a layer 1 or layer 2 protocol, which is an ecosystem that has promise and good user growth, but is typically plagued by inflationary tokenomics and low revenue. As these chains reach a higher level of maturity however, emissions will go down and revenue can increase, especially as more liquidity and applications come to each chain.

L2 Tradeoffs

The tradeoff that L2s typically make is finding ways to incorporate their token alongside Ether, especially when ETH is used to facilitate transactions as well as included in liquidity pairings with other tokens. They believe that this tradeoff is worth added security from posting transactions to the base layer of Ethereum while enjoying support from the Ethereum community as well.

DeFi Tokenomics

The year 2020 and onwards has seen the immense growth of Decentralized Finance (DeFi), and with it, many innovative token models to correctly balance incentives between governance token holders, liquidity providers and users.

The first iteration of tokens, however, ran into problems with a lack of utility and high inflation. Many projects launched tokens and simply designated them for governance and nothing else.

Of course, there is value to governance tokens, such as being able to vote on changes to an exchange that processes tons of volume and stores lots of liquidity, but it is limited as long as token holders have no access to revenue.

1. Uniswap

A great example of this is Uniswap, which has over four billion in TVL and processes billions in volume on a daily basis, in addition to claiming millions of dollars in fees. However, without fees being directed towards those who hold governance tokens, the claim that they “own” the platform is perhaps disingenuous since they see none of the revenue, all of which goes to liquidity providers. It is possible that fees will eventually be turned on for UNI holders, but the projected APR for staking relative to UNI’s market cap of 5.6 billion dollars will still be quite low, as the reported percentage of 0.05% of fees would not be enough to justify the valuation of the UNI token based on yield alone.

| Figma Community")

2. Trader Joe

Recent innovations in capital efficiency, however, have led to more possibilities for the use of Dex tokens. One example of this is Trader Joe, a Dex that was originally deployed on Avalanche and has since expanded to Arbitrum and soon to be on the Binance Smart Chain. Their novel liquidity book allows for the custom deployment of liquidity, such that LPs can structure their own liquidity as they see fit. This has resulted in the exchange becoming a magnet for stablecoin liquidity in particular, as LPs have seen huge APRs from the increased capital efficiency. In addition, Trader Joe shares revenue with those who stake their governance token JOE, adding further utility to the token outside of governance.

3. GMX and Gains

However, when it comes to capital efficiency, no decentralized exchanges have found success quite like decentralized derivative exchanges. Two examples of perpetual exchanges that have seen a massive increase in users and revenue are GMX, which is deployed on Avalanche and Arbitrum and have an identically named governance token, and Gains Network, which is deployed on Arbitrum and Polygon and has a governance token with the ticker GNS. Both of these have unique tokenomics to drive value to token holders and have been at the forefront of the “Real Yield” movement in DeFi which strives to reward token holders/stakers with revenue generated from the platform as opposed to token inflation, as was often the case in the recent bull market.

In the case of GMX, the goal was to incentivize sticky liquidity on the platform as well as reward early adopters of its governance token, all the while preventing token holders from dumping later on. Currently, 30% of the fees generated are routed to those who stake the GMX governance token. The protocol also instituted two things in particular: escrowed tokens and multiplier points. Escrowed tokens (esGMX) act as replicates of the original token but with a vesting period, in this case of an entire year, to become GMX tokens. This implementation allowed the protocol to attract liquidity at its inception without immediately flooding the market with newly minted GMX tokens. Multiplier points were a different innovation that were intended to reward long-term holders while simultaneously making it less optimal to sell tokens. By rewarding stakeholders with non-liquid tokens that increase yield but get burned every time a holder un-stakes their tokens, it ensures the highest yield is paid out to holders who have removed their tokens from circulation for the longest period of time.

The GNS token is similar in that those who stake it are rewarded with 32.5% of the fees generated, but differs in its implementation elsewhere. For one, there are no escrowed tokens or multiplier points to influence yield, but more importantly, its unique mechanism for minting/burning tokens allows GNS holders to act as counterparties to directional trades opened on the platform, compared to GMX where liquidity providers are the counterparty to traders. Since successful traders are paid out in Dai from the Gains Network Dai vault, the performance of traders directly impacts the collateralization of the Dai vault. In the event it dips below 100%, GNS tokens are minted and market sold to bring it back, whereas a collateralization of 130% triggers the market buying and burning of GNS tokens. In theory, this should make the GNS token long-term deflationary as short-term traders typically are net-negative in the market.

While these are just two examples of protocols that have found success with newer models that drive value to token holders, there are countless others that are following suit. It is possible that in DeFi, governance will be synonymous with not just the ability to vote on changes to the application, but being entitled to shares of its revenue as well.

Conclusion

As illustrated above, there are many different methods for creating digital economies based upon a platform’s native token, and there is not one correct way to do so. Whether it is creating a deflationary environment, incentivizing the locking of tokens to reduce liquid supply, distributing revenue, governance, or more, many tokens claim to be a solution to creating an ideal decentralized economy that rewards all participants. It will be fascinating to see which of these models stand the test of time and prove they are truly right about their claims.